Report: The Magnificent Seven

As the biggest-ever platform shift in modern technology unfolds, together with D...

Beyond understanding the corporate finance principles behind company valuation which we covered in the first two parts of our mini-series, it's insightful to develop an intuition on what drives market multiples which can be useful when putting the theory into practice - whether it's deal negotiation, assessing an investment opportunity or having a general view on the current state of market.

While the topics we've introduced so far are highly theoretical in nature, the first step to understanding the role between investor sentiment and market multiples is to further examine the impact that growth has on company valuations.

Perhaps the best way of exploring the impact of growth on company valuations is to look at an example of two (almost) identical listed companies. Let's call them FoodieA and FoodieB, and rather conveniently they have the same financials, management teams and prospects in the online food delivery market.

They both generated $100 million in revenue last year and are on track to deliver 10% growth in 2023 to reach $110 million this year. Assuming this is all common knowledge, it's safe to say that these companies should be identically valued by the market.

Now suddenly, it appears that the new marketing campaign for FoodieB has unexpectedly gone viral and new customers are flocking to this trendy service - and accordingly the revised revenue forecast for 2023 is now $125 million with a ripple effect on all the outer years. Having the choice to invest in either company, which one do you think would be the wiser investment?

Hopefully it's clear that FoodieB makes for a more attractive investment, since the future dividend stream will now be much higher (assuming all else stays equal). It's very likely that the market will push up the valuation to adjust for the company's new glowing prospects. Given that both companies had the same revenue in 2022, it follows that FoodieB will be trading at a higher revenue multiple than FoodieB.

We've already established that valuation multiples will be clearly impacted by anything that might impact future growth prospects of the business being evaluated. Therefore, various factors can impact valuations which are ultimately investors making a view on an optimal level of risk vs. return with a combination of firm-specific factors such as the management team and growth strategy as well as industry trends, competitive landscape and long-term defensibility.

Valuation multiples tend to be high for industry segments which have strong growth prospects such as early-stage startups where current financial performance only presents a limited view of the future revenue / EBITDA generation potential. Typically EBITDA multiples in excess of 100x are considered to be unrepresentative for any meaningful analysis.

Similarly, if there are aspects of an industry which are less desirable (and therefore considered to be riskier) such as tobacco or gambling - it's reasonable to assume that valuation multiples will be pushed lower from being considered an undesirable investment and the longer-term risk.

Early stage companies that have little or no profits have no choice but to be assessed purely on revenues. It's crucial that a basket of similar companies (same segment) are analysed for the analysis to make sense, since the long-term margin potential of a business will have a significant impact for revenue-based multiples.

As companies move towards a mature stage, EBITDA-based multiples are preferred since it captures the efficiency of the business - thereby presenting a more accurate view of the likely market valuation.

It's important to note that each industry might have specific characteristics that need to be considered. For example, advanced biotech companies undergoing clinical trials might already be listed, but valued on a multiple of their R&D spend due a lack of financial metrics.

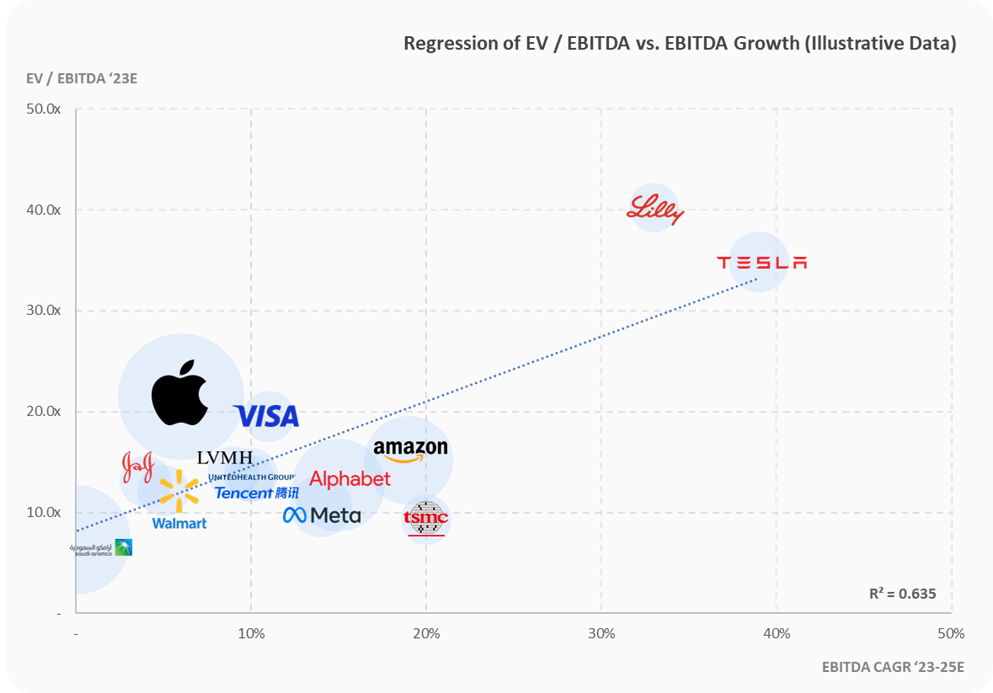

Let's take a look at some data to see how the link between growth and multiples works in practice. Does the theory hold up in the real-world and how significant is growth as a factor driving valuation?

As an example, let's take a selection of large-cap stocks and run a regression between the 2023-25E CAGR and EV / EBITDA 2023. Since we are mixing various segments in the regression, it's only insightful to run a regression on EBITDA rather than Revenue due to the variety in business models.

The regression confirms our expectations that growth drives EBITDA multiples higher given the R2 of over 0.6; although it's important to recognize that this is analysis is highly theoretical, hence why the correlation is far from perfect. However, we can still make some observations from the data.

The intuition explains how Tesla, a fast growing EV innovator which has only been profitable since 2020, is attracting a sky-high market valuation of almost 40x EBITDA due to rapid growth in future profit growth vs. Apple (a historic growth machine which has now matured).

And given a sufficiently sized sample, a trend line can be a potential indicator of what might be considered "fair-value" with companies that are above the line being relatively expensive vs. those companies trading below the line.

It's important to note that since we are mixing various industries in our analysis, we are inherently ignoring the fact that there may be market specific factors at play. And as our growth estimate is derived from stock analysts estimates between 2023 to 2025, it only captures a small portion of investor sentiment. Clearly missing is any consideration for outer years, especially for companies that are operating in high-growth industries.

As the biggest-ever platform shift in modern technology unfolds, together with D...

We are formally launching our tech sector coverage in Latin America, an ever-evo...

In conversation with Francisco Loehnert, co-founder and CEO of Awto, an autotech...

In conversation with Gabriela Estrada, co-founder and CEO of Vexi, a neobanking ...

2023 has been a wild ride in tech. From the rise of gen AI to public valuation m...

We checked in on the data and trends driving the global startup, tech and ventur...

We partnered with Dealroom to deliver the latest update on European tech ecosyst...

With the proliferation of new technologies comes the growing number and complexi...

Beyond understanding the corporate finance principles behind company valuation m...

Software as a Service (SaaS) business model has been around for a while, growing...

ARPPU, or 'Average Revenue per Paying User', is a measurement of the predicted r...

While most management teams tend to be overly optimistic when putting together f...

Company valuation is a key aspect of corporate finance that is used to determine...

South Korea is the fastest growing Asian Tiger nation for VC investment, and Seo...

Deliveroo is reported to target a $10B valuation in an upcoming IPO. In preparat...

In this report, we take a deep dive into the creator economy ecosystem to analyz...

Climate change is one of the most threatening crises of our time and the world n...

This was a pretty crazy year, to say at least. The COVID-19 health crisis, while...